The short answer: Access to lenders is not the main problem facing South African SMEs looking for funding. Readiness is. In our data, 50% of businesses applying for funding turn over less than R50,000 a month, which is below the minimum that almost every South African lender requires. Another large share have been trading for under a year. The result: 55% of applications are declined before they ever reach a lender, almost always for reasons the business owner could fix. This report breaks down exactly what lenders look for, where applicants fall short, and the practical path from “not yet” to “approved” — in short, how to build funding readiness.

What we looked at

Over the course of 2026, more than 1,000 SMEs have applied for funding through our Funding Desk, and hundreds of them in the last month alone. Demand for business finance in South Africa is clearly strong and growing. Every applicant told us their monthly turnover, how long they have been trading, and how much they were looking to raise. That gives us an unusually honest, ground-level view of who is actually seeking capital, and why so many struggle to secure it. SME South Africa has connected business owners with funders and business-support partners for over a decade, which is what lets us read these patterns across the whole market rather than through a single lender book of business.

Finding 1: Half of applicants earn below the lender minimum

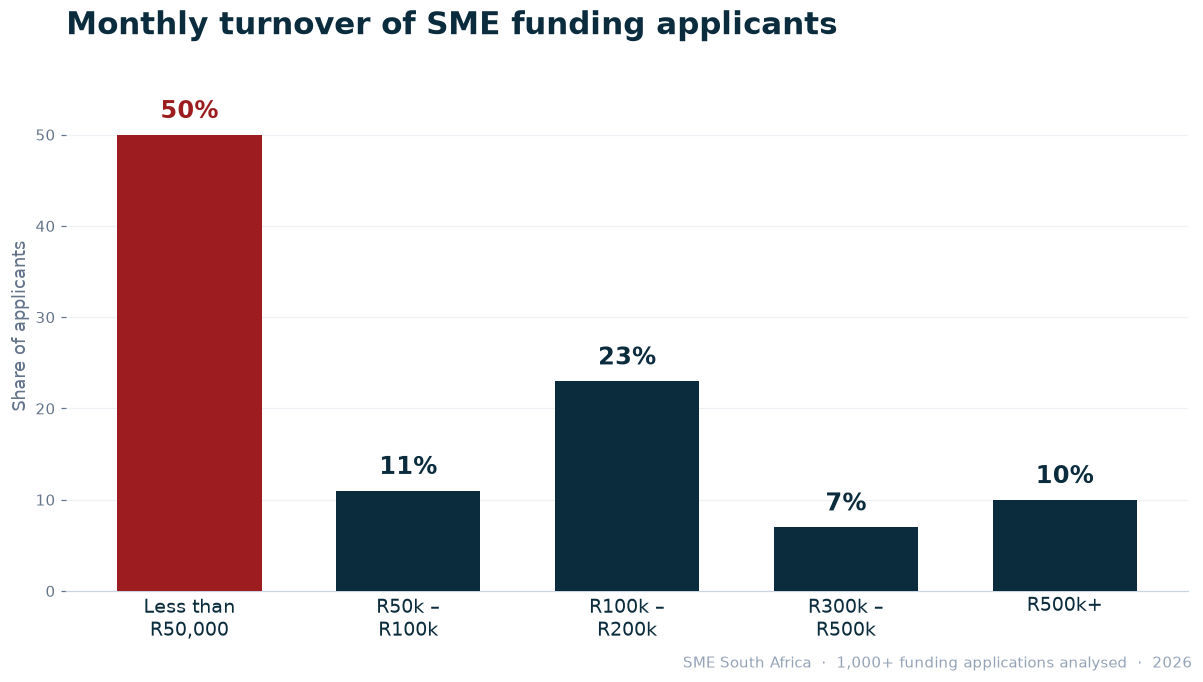

The single biggest barrier is revenue. Here is how monthly turnover breaks down across more than 1,000 applications:

| Monthly turnover | Share of applicants |

|---|---|

| Less than R50,000 | 50% |

| R50,000 to R100,000 | 11% |

| R100,000 to R200,000 | 23% |

| R300,000 to R500,000 | 7% |

| R500,000 and above | 10% |

Half of all applicants, one in every two, turn over less than R50,000 a month. That matters because R50,000 a month is roughly the floor most South African lenders will consider. A business under that line is not being rejected because lenders are difficult; it simply has not yet reached the revenue that funders can lend against responsibly.

Finding 2: Many businesses are still very young

Lenders also want to see a trading history, usually 6 to 12 months of bank statements at a minimum. Yet 22% of applicants have been in business for under a year, and a further chunk are in their first two years. Young businesses are the lifeblood of the economy, but a lender needs enough history to see that income is real and repeatable before advancing money against it.

Finding 3: 55% are declined at first screening

Put those two facts together and the outcome is predictable: 55% of applications are declined at the first screening stage, before they are ever sent to a lending partner. When we look closer, the declines cluster around the same handful of fixable issues:

- Turnover below R50,000 a month, the number one reason.

- Under 6 to 12 months of trading history.

- Bank statements that cannot be read or verified, often photographed or scanned images rather than the bank’s official PDF, so income cannot be confirmed.

- Missing or invalid company registration (CIPC).

- Affordability once existing debt is counted, when current loans and debit orders leave too little of the income free to service anything new.

- Returned debit orders or an overdrawn account on the recent statements, which read as cash-flow strain.

- Income that is irregular or highly seasonal with no buffer, so a lender cannot count on a repayment clearing each month.

- A recent application to the same lender, or an existing facility already in place — many funders will not look at a fresh application within a few months of a previous one.

- A credit issue in the owner’s or director’s personal profile, since lenders check the people behind a young business, not only the business itself.

When a lender or our own desk declines an application, the reason that comes back is almost never that the business is a bad idea. It is one of the items above: the numbers are not there yet, the history is too short, or the account tells a story of strain. None of these are about the idea or the industry. They are about readiness, and every one of them is something an owner can work on.

What lenders in South Africa actually require

If you want to know whether you are fundable, measure yourself against what the major South African business lenders genuinely ask for. The bar varies by lender, which is why matching matters:

| Lender | Minimum monthly turnover | Trading history |

|---|---|---|

| Lula | around R40,000 | 12 months |

| Retail Capital | around R50,000 | 12 months |

| Genfin | around R100,000 | 12 months (registered companies) |

| SourceFin (purchase-order funding) | Funds the order value, from R250,000 per PO | A confirmed purchase order |

Across the board, the common thread is this: at least around R50,000 a month in turnover, at least 12 months of trading, and clean, verifiable bank statements that show regular transactions. Purchase-order funding is the exception: with a confirmed order of R250,000 or more from a credible buyer, SourceFin can fund the order value even without a long trading history. Meet those, and you move from “declined at screening” to “matched with a lender.”

The path from “not yet” to “fundable”

If your application is not ready today, here is the practical route to becoming fundable. Most SMEs can get there in a few months of focused work:

- Grow toward R50,000 a month in turnover. This is the biggest lever. Even reaching a consistent R50k opens up the majority of lenders.

- Bank everything through the business account. Lenders assess your bank statements, not your word. Cash sales that never touch the account are invisible to a funder, and they cost you.

- Keep 6 to 12 months of clean statements. Download the official PDF from your bank (not a photo or screenshot) when you apply. Unreadable statements are a common, avoidable decline.

- Register with CIPC and keep the company in good standing. It is a basic gate for most formal lenders.

- Show steady, recurring income. A spread of regular transactions reads as a healthier business than one or two large lump sums, unless you have a strong single client, in which case say so.

- Only ask for what your turnover supports. A request that dwarfs your annual revenue is a red flag; a modest, well-justified amount is approved far more often.

Get your books in order while you are at it. A business with clean, up-to-date financials is far easier to fund, and to run. And if you are very early-stage and still below the private-lender bar, government-backed option such as Sedfa is worth exploring while you build up.

The other half: businesses that are ready

It is not all a readiness gap. A meaningful share of applicants, the 10% turning over R500,000 or more a month, and many in the R100k to R200k band, are exactly what lenders are looking for. For these businesses, the challenge is not qualifying; it is getting matched to the right lender quickly so a fixable cash-flow gap or growth opportunity does not pass them by. The most common amounts requested sit between R150,000 and R1 million, solid, fundable working-capital sums.

The bottom line

The story South Africa’s SME funding data tells in 2026 is hopeful, not bleak. The appetite to grow is huge, with hundreds of businesses actively seeking capital every quarter. The barrier for most is not a closed door; it is a readiness gap that owners can close themselves: reach R50k a month, bank through the business, keep clean statements, and stay registered. Do that, and funding stops being a wall and becomes a step.

If you are not sure where you stand, the fastest way to find out is to be assessed. Our Funding Desk reviews your figures against real lender criteria and tells you honestly whether you are ready, and if not, exactly what to fix.

Get your free funding readiness check

Frequently asked questions

How much monthly turnover do I need to qualify for business funding in South Africa?

Most private lenders start at around R50,000 a month, though it varies: Lula from about R40,000, Retail Capital around R50,000 and Genfin around R100,000. Below roughly R50,000 a month, the priority is growing revenue and banking it through the business.

Can I get funding if my business is less than a year old?

It is harder, because most lenders want 6 to 12 months of bank statements. Purchase-order funding (for a confirmed order of R250,000 or more) and government-backed options are the main routes for very young businesses.

Why was my funding application declined?

The most common reasons are turnover below the lender minimum, too short a trading history, bank statements that cannot be read or verified, missing CIPC registration, and affordability once existing debt is taken into account. Almost all of these are fixable.

What is funding readiness?

Funding readiness is the state of meeting what lenders actually check before they will consider you: enough monthly turnover, a clean and verifiable trading history, valid registration, and a request sized to your revenue. This report is a guide to reaching it.

Methodology: figures are drawn from more than 1,000 business-funding applications submitted via SME South Africa in 2026. Turnover and trading-history figures are as reported by applicants; decline figures reflect first-stage screening against lender eligibility criteria. Data is aggregated to protect applicant privacy. Last updated: July 2026.